ARCHIVED – Canada’s Energy Futures 2018 Supplement: Oil Sands Production

This page has been archived on the Web

Information identified as archived is provided for reference, research or recordkeeping purposes. It is not subject to the Government of Canada Web Standards and has not been altered or updated since it was archived. Please contact us to request a format other than those available.

Canada’s Energy Futures 2018 Supplement: Oil Sands Production [PDF 1428 KB]

Data and Figures [EXCEL 709 KB]

May 2019

Copyright/Permission to Reproduce

ISSN 2369-1476

Table of Contents

Chapter 1: Background

The National Energy Board’s (NEB) Energy Futures (EF) series explores how possible energy futures might unfold for Canadians over the long term. EF analyses consider a range of impacts across the entire Canadian energy system. In order to cover all aspects of Canadian energy in one supply and demand outlook, the extensive crude oil, natural gas, and natural gas liquids (NGL) production analyses are described at a relatively high level. A series of supplemental reports is able to address impacts specific to the supply sector, creating an opportunity to provide additional detail.

Future oil prices are a key driver of future oil production and a key uncertainty to the projections in the Canada’s Energy Future 2018: Energy Supply and Demand Projections to 2040 (EF2018). Crude oil prices could be higher or lower depending on demand, technology, geopolitical events, and the pace at which nations enact policies to reduce GHG emissions.

EF analysis assumes that, over the long term, all energy produced will find markets. In the near-term, a lack of available pipeline export capacity was accounted for in the price assumptions for western Canadian crudes. The timing and extent to which particular markets emerge, whether demand growth over/undershoots local production, whether export/import opportunities arise, and whether new transportation infrastructure is built, are difficult to predict. This is why simplifying assumptions are made. The analysis in this supplemental report continues the EF tradition of assuming these short-term disconnects are resolved over the longer term.

The EF series of Natural Gas, Crude Oil and NGL supplement reports include four EF cases.

Table 1.1 EF2018 Natural Gas and Crude Oil Production Assumptions/Cases

| Variables | Reference | High Price | Low Price | Technology |

|---|---|---|---|---|

| Oil Price | Moderate | High | Low | Moderate |

| Gas Price | Moderate | High | Low | Moderate |

| Carbon Price | Fixed nominal C$50/t | Fixed nominal C$50/t | Fixed nominal C$50/t | Increasing CO2 cost reaching nominal C$336/t in 2040 |

| Technology Advances | Reference assumption | Reference assumption | Reference assumption | Accelerated |

| Notes | Based on a current economic outlook and a moderate view of energy prices | Since price is one of the most influential factors in oil and gas production, and does vary over time, these two cases look at the effects of significant price differences on production | Considers the impact of greater adoption of select emerging energy technologies on the Canadian energy system, including technological advances in oil sands production; and the impact on the Canadian energy system of higher carbon pricing | |

Alberta’s oil sands will be responsible for the majority of crude oil production in Canada through 2040 in all four cases, mainly because of growing in situ production. This supplemental report provides additional analysis and results of EF2018’s four cases. Differences in production forecasts between the cases are because of different oil price assumptions and new technologies used for in situ development in the Technology Case.

The Appendix describes methods and assumptions used to project production, and provides detailed data sets for all cases. These include monthly production by oil sands region, monthly production by method of extraction, and whether the production is from existing, expanded, or new projects. The data used in this supplemental report as well as from the appendices are available here [EXCEL 709 KB].

Chapter 2: Results – Reference Case

2.1 Production by Oil Sands Region

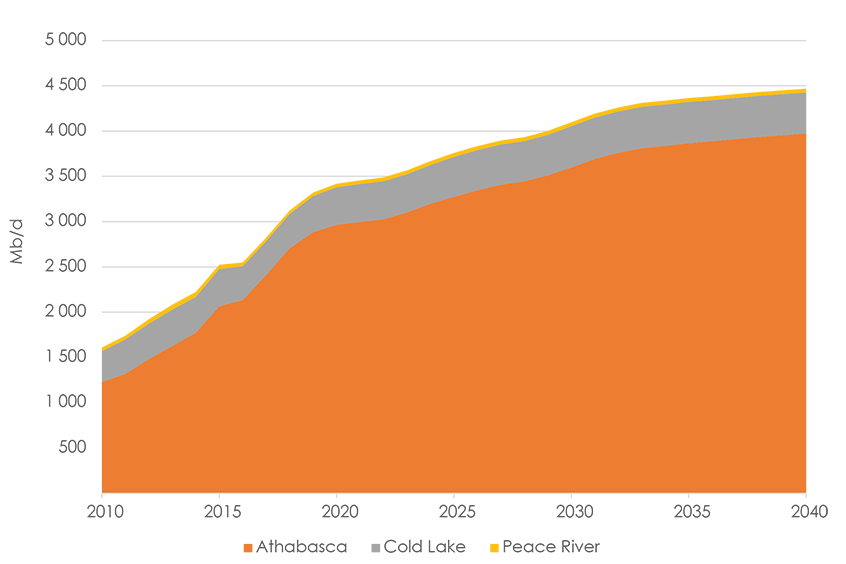

Figure 2.1 Raw Bitumen Production by Region

Description:

This graph presents raw bitumen production for the Reference Case in each of the three oil sands areas, Athabasca, Cold Lake and Peace River. The Athabasca region continues to be the largest contributor to total oil sands output, reaching 4.0 MMb/d, or 89%, by 2040. Cold Lake continues to increase production over the projection period reaching 0.45 MMb/d, or 10%, by 2040 while Peace River production falls to 0.04 MMb/d, or 1.0%, by 2040.

- Oil sands production has increased in recent years. This is largely because projects that started construction prior to mid-2014’s crude-oil price collapse have been completed and came online. This trend will continue into the early 2020s, after which production will grow more slowly. In 2017, WTI oil prices averaged US$50.80 per barrel which, when netted back to western Canada, was high enough to cover operating costs of existing projects and spur investment in some new projects. As WTI prices rise, reaching US$71.50 per barrel by 2027, additional investment in the oil sands occurs. This leads to higher growth rates in the second half of the next decade. Oil sands production in 2017 was just over 2.8 million barrels per day (MMb/d) and will reach just under 4.5 MMb/d in 2040, a 58% increase.

- The Athabasca region produces the majority of oil sands raw bitumen, both historically and throughout the projections (Figure 2.1). Averaging 2.4 MMb/d in 2017, the Athabasca region produced 85% of all raw bitumen, with Cold Lake and Peace River producing 13% per cent and 1% respectively.

- Most of the mined bitumen as well as some in situ production is upgraded in Alberta into synthetic crude oil. There are exceptions, however. Fort Hills—which came online in late 2017—and Kearl both produce diluted bitumen, which is transported to markets by pipeline or rail.

2.2 Production by Extraction Method

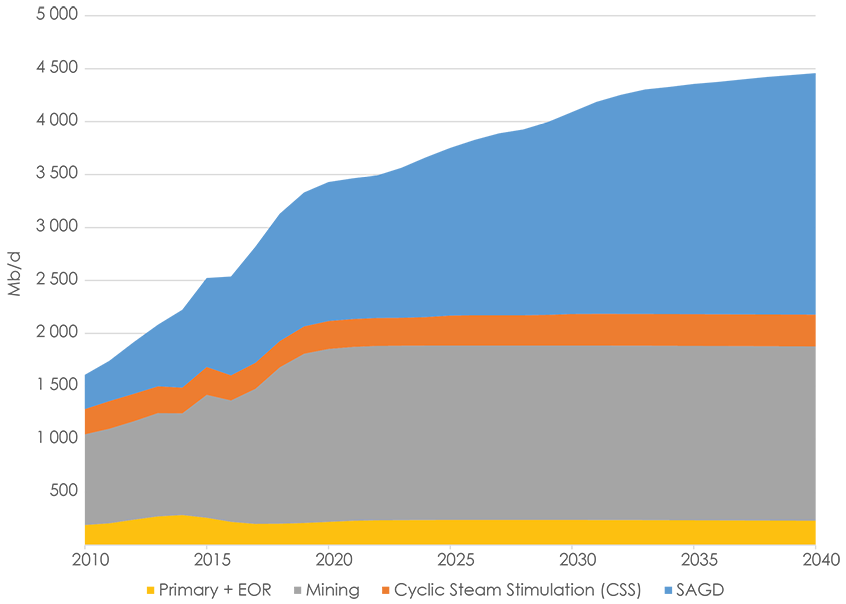

Figure 2.2 Raw Bitumen Production by Extraction Method

Description:

This graph shows the proportion of raw bitumen production attributable to each of four main extraction methods: Mining; Steam Assisted Gravity Drainage (SAGD); Cyclic Steam Stimulation (CSS); and Mining and Primary/Enhanced Oil Recovery (EOR). Production from both SAGD and CSS continue to grow reaching 2.6 MMb/d by 2040 while primary and EOR production increases early in the projection to 0.30 MMb/d by 2025 before declining to 0.23 MMb/d by 2040. Mined production reaches 1.6 MMb/d in 2022 and remains relatively stable for the remainder of the projection period.

- Bitumen is produced in Alberta in one of three ways:

- Surface mining, using trucks and excavators (referred to as “truck and shovel”).

- In situ, which primarily uses steam to heat the reservoir, allowing the bitumen to be pumped to the surface through horizontal wells. This can be either Steam Assisted Gravity Drainage (SAGD) or Cyclic Steam Stimulation (CSS). In the future, injecting solvents with steam or instead of steam are expected to play an increasingly important role in in situ production.

- Primary production and enhanced oil production (EOR), which produces the bitumen like conventional oil wells and requires no steam.

- Mining is currently used to develop oil sands deposits up to a depth of about 70 meters. Most historical development of the oil sands has been through mining. However, only about 20% of oil sands deposits can be accessed this way.

- The remaining 80% of oil sands deposits can only be developed with in situ technology. In 2012, in situ production surpassed mining production and is now the largest source of crude oil in Canada. In situ production is expected to continue growing faster than mining production and will account for 58% of all raw bitumen production by 2040.

- Figure 2.2 shows mining production will plateau after new and expansion projects currently being developed are ramped up to full production, which is typically 90% of nameplate capacity. Only relatively small additions to mining are expected to come online thereafter, entirely through expansions to existing facilities. Mined production reaches 1.65 MMb/d in 2022 and remains relatively stable for the remainder of the projection. Typically, producers develop the best area of their land first, then step into lower quality areas as the operation matures. This projection assumes processes and technology will continue to improve to offset declines in bitumen production from developing lower quality reservoir, keeping mined production relatively stable.

- Costs to operate or expand existing in situ facilities, as well as build new in situ facilities, are expected to continue improving. This leads to growing in situ production from both SAGD and CSS, reaching 2.58 MMb/d by 2040.

- Primary and EOR production remains relatively stable throughout the forecast, peaking in 2025 at 0.24 MMb/d before declining to 0.23 MMb/d by 2040.

2.3 New and Legacy Bitumen Production

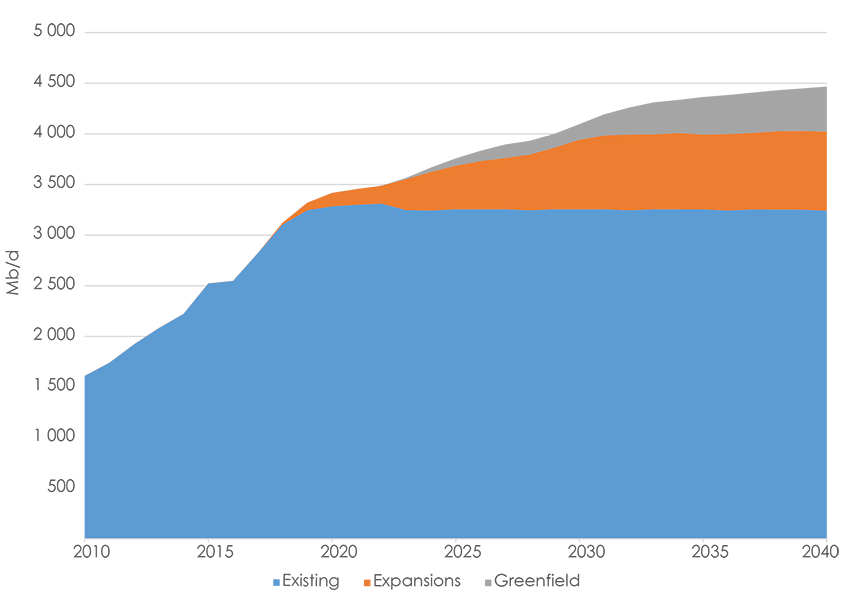

Figure 2.3 New and Legacy Production

Description:

This graph shows production of raw bitumen by existing, expansion and entirely new or greenfield projects for the projection period. Production from existing projects increases slightly over the projection period because of process and technology improvements and the ramp-up in production from projects that have yet to reach full capacity, reaching 3.2 MMb/d by 2040. Expansions will account for 17% or 0.8 MMb/d by 2040 while 0.5 MMb/d or 10% of total production will come from greenfield projects.

- Because bitumen projection from mining and in situ projects does not decline like production from conventional oil wells, bitumen production currently online will remain steady over the projection period.

- Production averaged just over 2.8 MMb/d from mining, in situ, and primary/EOR combined in 2017. Figure 2.3 shows current projects slightly increase their production over the projection period because of process, improvements, technology improvements, and projects not yet at full capacity ramping up their production. Total production from current projects reaches 3.24 MMb/d by 2040.

- The largest contributor to oil sands production growth will be expansions to existing in situ facilities. At 0.78 MMb/d, expansions will produce 64% of new production by 2040.

- Entirely new projects (i.e. greenfield projects) will produce the remaining 36% of new production and will produce 0.45 MMb/d by 2040. This relatively small share is because greenfield projects are typically more expensive to build than expansions.

2.4 Production by Project

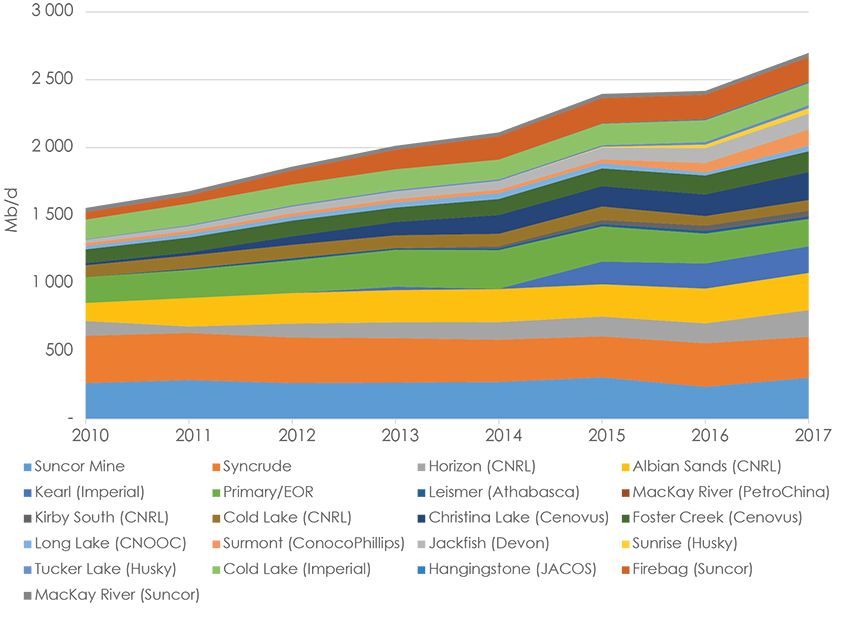

Figure 2.4 Raw Bitumen Production by Project

Description:

Historical production (2010-2017) from each project is shown in this graph. Average annual production rose from 1.6 MMb/d in 2010 to 2.8 MMb/d in 2017. Mining accounted for over 51% of all production in 2010 falling to 45% in 2017 with the remaining production coming from in situ and primary/EOR methods.

- Projects individually shown in Figure 2.4 have capacities exceeding 20 000 barrels per day. All other projects are grouped into “Other”

- Average annual production rose from 1.6 MMb/d in 2010 to over 2.6 Mb/d in 2016 from these projects.

- Mining produced 51% of all raw bitumen in 2010, though this fell to 42% in 2016 with the remaining bitumen coming from in situ and primary/EOR projects.

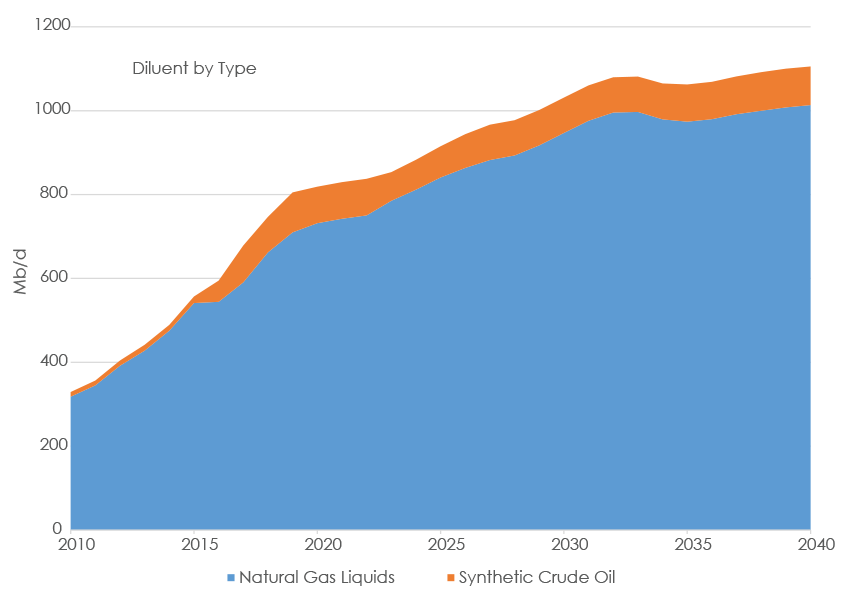

2.5 Diluent Requirements

Figure 2.5 Diluent Requirements

Description:

This graph shows diluent requirements for oil sands and heavy oil. Natural Gas Liquids (NGL) are the most widely used diluent and grow from 0.6 Mb/d in 2017 to 1.01 Mb/d in 2040. Synthetic crude oil is also used as a diluent, though less so. Synthetic crude oil as a diluent remains stable at 0.09 Mb/d.

- With few exceptions, bitumen must be blended with a lighter hydrocarbon (i.e., diluent) so it can flow within pipelines or be carried on train cars. The most common form of diluent is Natural Gas Liquids (NGL), though synthetic crude oil and other light oils are also used.

- The amount of diluent required to blend bitumen varies depending on the type of diluent and the mode of transportation. Typically, bitumen blended with NGLs for shipping in pipelines requires roughly 1 barrel of NGL for every 3 barrels of diluted bitumen, or a 30% blend ratio. If the diluent is synthetic crude oil, then more diluent is required, about 1 barrel for every 2 barrels of diluted bitumen. However, relatively few oil sands operations use synthetic crude oil or other light oils as diluent.

- Figure 2.5 shows the amount of diluent the oil sands will require over the projection period. Synthetic crude oil is increasingly used as a diluent early in the projection, reaching 0.10 MMb/d in 2019 before flattening. NGL use as a diluent, however, grows considerably over the projection, jumping 72% to reach 1.01 MMb/d by 2040

Chapter 3: Results – All Cases

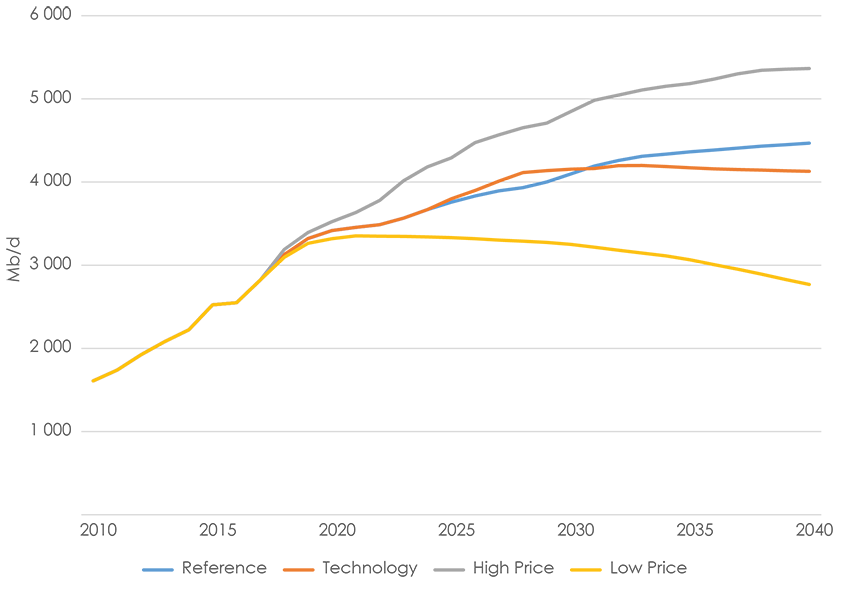

Figure 3.1 Raw Bitumen Production from all four EF 2018 Cases

Description:

The graph shows the variety of results in production from all four EF2018 cases. In order of volume of raw bitumen production in 2040, the results of the analysis are as follows: 2.8 MMb/d in the Low Price Case, 4.1 MMb/d in the Technology Case, 4.5 MMb/d in the Reference Case and, 5.4 MMb/d in the High Price Case.

- To capture the uncertainty in projecting oil production until 2040, a wide range of future prices were assumed. WTI prices reach US$116.50 per barrel in the High Price Case and decline to US$36.50 in the Low Price Case. In 2040, bitumen production would be 5.37 MMb/d in the High Case and 2.77 MMb/d in the Low Case (Figure 3.1).

- Similar to last year’s Technology Cases, this year’s Technology Case assumes steam solvent technologies are more quickly adopted in the oil sands. Other innovations, such as wedge wellsNote de bas de page 1 and flow control devicesNote de bas de page 2, are also assumed to be more widely adopted early in the projection. In this case, these technologies lower overall GHG emissions intensity from the oil sands while increasing production of many facilities at the same time.

- Figure 3.1 shows how widespread adoption of these technologies affects production. Production in the Technology Case grows quicker than the Reference Case early in the projection, reaching 4.20 MMb/d by 2033 before falling slightly to 4.13 MMb/d by 2040. The early peak and subsequent fall of production in this case is because lower price assumptions, coupled with increased carbon pricing, eventually completely offset the early production increase brought on by technology improvements.

Chapter 4: Considerations

- Future oil prices are a key driver of future oil production and a key uncertainty to the projections in EF2018. Crude oil prices could be higher or lower depending on demand trends, technological developments, geopolitical events, and the pace at which nations enact policies to reduce GHG emissions.

- This analysis assumes that, over the long term, all energy production will find markets and infrastructure will be built as needed. In the near-term however, a lack of available pipeline capacity impacts pricing of Canadian crude oil and the economics of production.

- The Technology Case assumes global crude oil prices are lower than in the Reference Case. Future prices in a GHG-constrained world are uncertain and depend on how robust concerted global climate action is, how oil demand responds to higher carbon prices, and alternatives to existing technology.

- Efforts to increase efficiency and decrease costs and environmental footprint in the oil sands are another key uncertainty in EF2018’s projections. Should technology advance at a different pace than assumed, then projections of bitumen production would change accordingly.

Appendix

Appendix A

Projecting Oil Sands Production: Methods

Oil sands production is projected by applying utilization rates to the capacities of existing oil sands projects and the timelines of new projects and expansion phases expected to be built in the future. Projections do not consider changes to production as a result of weather, equipment failure, or other potential interruptions. Raw bitumen production and synthetic crude oil production are projected for each case.

The main differences between the cases are oil prices, carbon taxes, and technology assumptions. Varying oil prices affect industry revenues, and the reinvestment of a portion of the revenue as capital expenditures. Varying carbon taxes affect the net revenue available. The higher the carbon taxes, the higher the cost of production and the lower the net revenue. Technological advancements affect both bitumen production, as well as the steam to oil ratio (SOR). These variations do not affect all oil sands projects uniformly. For instance, the better a project’s SOR, the less impact rising carbon taxes have. This results in an emissions credit for some projects in some years. More details about how emissions are calculated are provided in Section A4.4.

Mining and in situ production are estimated using the same method. Projects are assessed based on their announced capacities and start dates and then risked in terms of start time. Production from all projects of each type (i.e. mining, in situ) is then aggregated. Production from projects that are currently operating is held relatively constant for the majority of the projection. In some cases, depending on the age of the facility, production is decreased towards the end of the projection period. Increases in production for any given project are largely the result of new phases coming online and, to a lesser extent, process improvements in the early years of that project or phase. These methods significantly differ from conventional oil projections, which are well-based and use decline-curve analysis.

Details on oil sands producing areas are in Appendix A1.1. How production is determined is discussed in Appendix A1.2. Projection results can be found in Appendix B [EXCEL 709 KB].

A.1 Oil Sands Production Categories

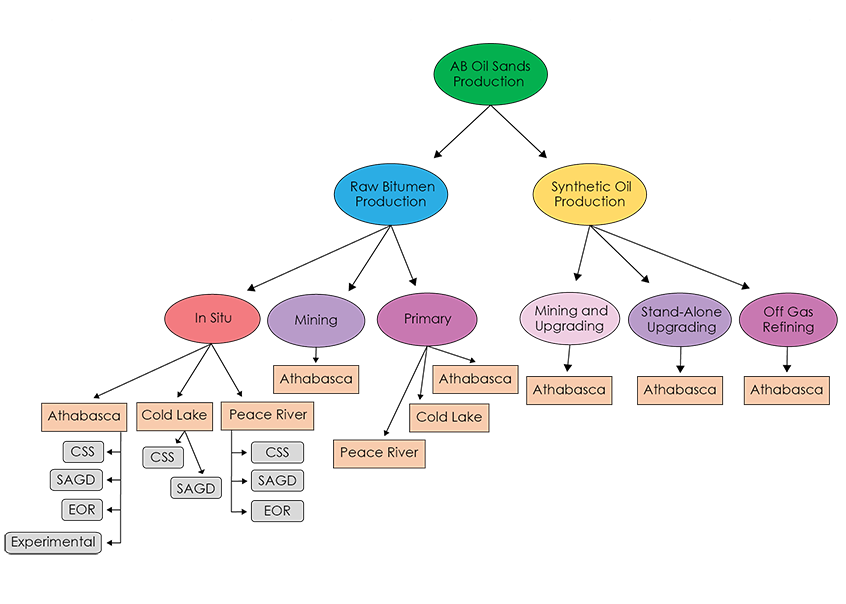

For this analysis, oil sands production is categorized by type of production, type of recovery, geography, and recovery method. Figure A.1 shows the breakdown.

Figure A.1 – Oil Sands Production Categories

Description:

This figure shows a flow chart depicting the breakdown of components that are analyzed to reach a projection of raw bitumen production. The same process is used for each of the cases. Raw bitumen production is projected for each type of production facility (Experimental, EOR, SAGD, CSS, Mining) within each of the three oil sands regions (Athabasca, Cold Lake, Peace River) where applicable. The results of this work is then aggregated to form the projection for total raw bitumen production. Synthetic crude oil is also forecast and is a combination of mining and in situ production that is upgraded within Alberta.

A.1.1 Oil Sands Areas

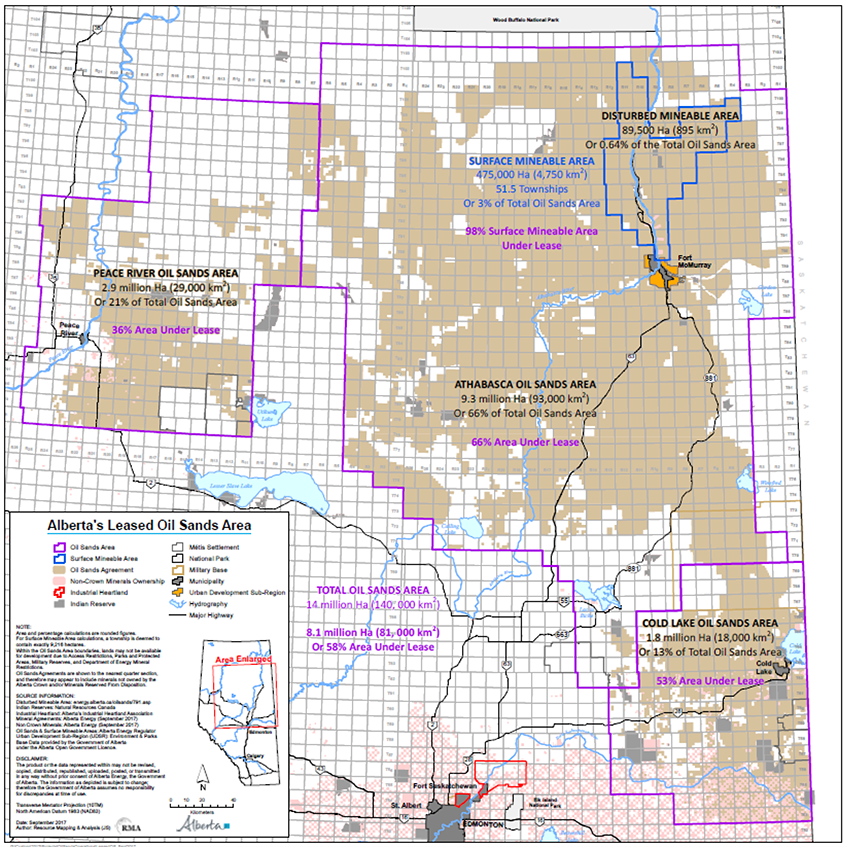

Oil sands production occurs in three areas in Alberta: Athabasca, Cold Lake, and Peace River. Athabasca has the majority of activity and production, including SAGD, CSS, and EOR in situ projects. Athabasca also has mining projects, upgrading, off gas refinery projects, and primary projects. Cold Lake has SAGD and CSS in situ projects, as well as primary projects. Peace River has SAGD, CSS, and EOR in situ projects and primary projects.

Figure A1.1 – Oil Sands Areas Map

Description:

This figure contains a map showing the aerial extent of each of the three oil sands areas, Athabasca, Cold Lake and Peace River.

A.1.2 Type of Production – Raw Bitumen and Synthetic Crude Oil

Both raw bitumen production and synthetic crude oil production are projected as part of the analysis. The majority of mined bitumen is upgraded within Alberta with some notable exceptions. In addition, production from two in situ facilities, Suncor’s Firebag and MacKay River projects, is partially upgraded to synthetic crude oil. The remaining volumes of in situ production, as well as production from Imperial’s Kearl Mine Suncor’s Fort Hills Mine, are marketed as diluted bitumen.

A.1.3 Type of Recovery – In Situ, Mining, Primary, EOR

Bitumen is produced in one of four ways. Roughly 90% is either mined or extracted using in situ methods. Remaining production comes from Primary and Enhanced Oil Recovery (EOR). Primary bitumen production is slightly less viscous than in situ bitumen and can flow to the surface without applying heat or solvents. However, these projects are of a smaller scale than in situ developments. EOR uses reservoir flooding similar to the technology used for conventional oil. These too are smaller scale than either mining or in situ projects. Combined, there were over 150 Primary and EOR projects operating within Alberta in 2017.

A.1.4 In Situ Recovery Method – SAGD, CSS, EOR

There are three types of in situ recovery technologies included in this report: SAGD, CSS, and EOR.

SAGD typically uses pairs of horizontal wells to produce bitumen. Steam is injected into an upper well to heat the bitumen, which then drains by gravity into a lower well and is pumped to the surface.

CSS also uses steam to produce bitumen. The steam is injected into a reservoir through a well over a period of several months, heating and decreasing the bitumen’s viscosity. Later, the steam is turned off and the emulsion of water and bitumen flows back into the well over a period of several months. The process is repeated for the economic life of the well.

EOR extracts oil from reservoirs once pressures have fallen to a point where natural production is no longer economically viable, even with artificial lifts like pump jacks. This includes pressure maintenance, cycling, water flooding, thermal methods, chemical flooding, and the use of miscible and immiscible displacement fluids.

A.2 Methods to Project Bitumen Production

For this report, historical production data, plans announced by producers, and industry and government consultations were used to derive projections. Monthly projections out to the end of 2040 are made for existing projects, for future (new) projects, and for expansions of both existing and new projects.

A.2.1 Method for Existing Projects

Projects that are, or have, produced are categorized as existing projects and their historical monthly production trend is used to project future production. For the most part, existing projects’ production is held constant out to 2040. Projections for projects whose production is currently declining maintain that decline. Projects whose production is currently zero but produced in the past will either have zero production over the projections (retired projects) or return to the expected levels at a given time based on publicly available information (i.e., projects that have been temporarily shut down).

A.2.2 Method for Expansions

Expansions are additions to existing projects. Given the oil price assumptions, most future increases in bitumen production will come from expansions of existing projects rather than new projects. Publically available information is used to determine the size and timing of expansions.

A.2.3 Method for Future Projects

Given a projected oil price and other assumptions, it may be warranted to include one or more new projects in the projection. New in situ projects are expected to be built as well though the timing, size and number of projects differs between the cases.

A.3 Synthetic Crude Oil Production Projection Methods

Synthetic crude oil is raw bitumen that is processed into a lighter crude oil. Most mined bitumen is currently upgraded and it is assumed this trend will continue throughout the projection period. In addition to mining, some in situ and heavy oil production is upgraded.

A.4 Diluent Requirements

Diluent requirements are estimated by taking into account the annual average blending ratios for each individual oil sands project. This ratio varies by type of heavy crude oil being blended and the type of diluent being used. The volume of diluent required to blend conventional heavy oil (i.e. all heavy oil not produced by the oil sands) is also included in this analysis.

A.5 Other Assumptions and Analysis

A.5.1 CO2 Assumptions

The cost of carbon dioxide emissions are included in the analysis. The cost of emissions decreases industry revenue and cash flow available for future capital expenditures. However, on a project by project basis, the cost of carbon may or may not affect the production projection. More efficient projects with lower SORs won’t have their economics affected as much as less efficient projects. Thus, for most projects, given current and projected SORs, the production projection is the same Note de bas de page 3 for varying carbon prices. Less efficient, usually smaller, projects are assumed to be affected with some production taken out of the projection given the carbon and oil price assumptions.

The amount of gas consumed, and CO2 emitted, can be calculated using the gas use per barrel of bitumen or synthetic oil discussed in section A.4.2. The assumed ratio is:

0.0019 tonnes of CO2 / m3 of natural gas use

An output-based adjustment, as based on Alberta’s climate plan, was then applied to the actual cost of CO2, for each project by year. For a given year, the projects are ranked from lowest SOR to highest SOR. The 25th percentile lowest SOR is a threshold level. The carbon cost associated with that SOR is the output-based adjustment and all projects’ carbon costs are adjusted by that amount. Thus, the projects with lower SORs than the threshold end up with a carbon cost less than zero (revenue is adjusted up) and the rest of the projects have lower, but still positive carbon costs (revenue is adjusted lower). More information on carbon calculations and provincial policies can be found in the Energy Future 2018 report.

Appendix B

Appendix B – Detailed Data Tables

Data for the figures in Appendices A and B are available in a Microsoft Excel file [EXCEL 709 KB].

- Date modified: