ARCHIVED - Energy Supply and Demand in a Pandemic: Effects of COVID-19

This page has been archived on the Web

Information identified as archived is provided for reference, research or recordkeeping purposes. It is not subject to the Government of Canada Web Standards and has not been altered or updated since it was archived. Please contact us to request a format other than those available.

The COVID-19 coronavirus was first identified in December 2019 and by March 2020, the virus had spread around the world, including Canada. To protect the health of their citizens, governments tried to limit the virus’s spread, including by encouraging social distancing, imposing travel restrictions, and closing businesses to reduce the gathering of crowds.

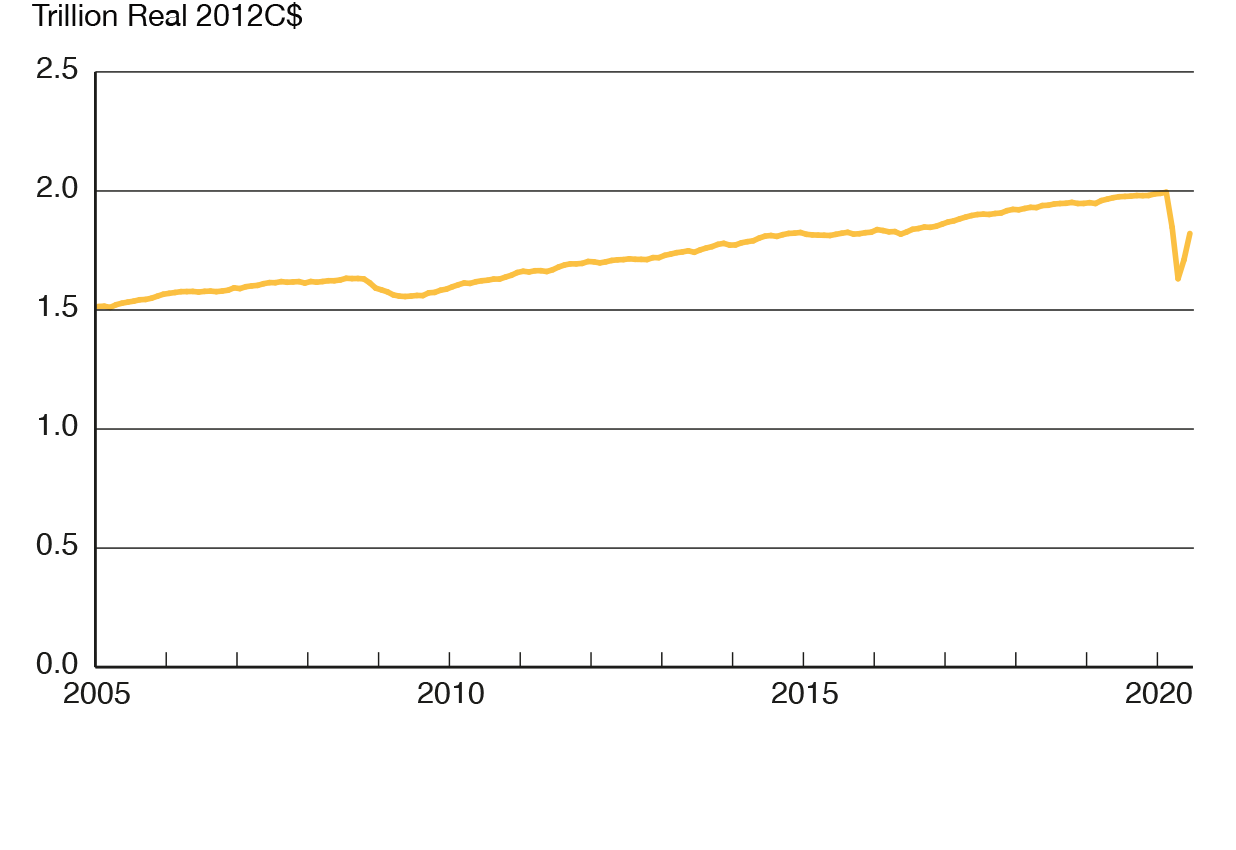

The impact on Canada has been significant. As shown in Figure C.1, Canada’s gross domestic product (GDP) shrunk in March and April 2020 by 19% to a level not seen since 2010. For the whole of 2020, Canada’s economy could shrink the most since the Great Depression of the late 1920s and 1930s.

Actions to reduce the spread of COVID-19, and the associated economic impacts, have had a significant impact on the Canadian energy system. The following section discusses the short-term market impacts of COVID-19 followed by the long-term uncertainties for the Canadian energy system resulting from the pandemic.

Description

Description

Description

This figure shows monthly Canadian gross domestic product in trillion $2012 C$, from 2005 to 2020. GDP generally grows steadily over this period, with a significant decrease in 2008 and 2009 associated with the global financial crisis, and a sharp drop in 2020 due to the COVID-19 pandemic.