Market Snapshot: Historical Trends in Canadian Oil and Gas Investment

Connect/Contact Us

Please send comments, questions, or suggestions for Market Snapshot topics to snapshots@cer-rec.gc.ca

Release date: 2022-11-23

Canadian oil and gas investments have historically changed along with energy prices. These investments vary by type of resource, such as conventional oilDefinition* versus oil sands,Definition* and by region. Investments in Canadian oil and gas are rising from their 2020 lows due to higher prices. But other factors are becoming more important for the industry, such as environmental, social, and governance (ESGFootnote 1) considerations and net-zero emissions policies.

Investments are linked to global markets and trends

Typically, Canadian oil and gas investments fluctuate with global industry cycles – although access to transportation infrastructure is a distinctively Canadian challenge. These cycles are driven by global economic activity, supply and development costs of oil and gas resources, and commodity prices.

Rising prices and an economic slowdown

From the early 2000s to 2008, concerns of supply shortage led to rising oil and gas prices globally and in North America. With rising prices, Canadian oil and gas investment levels hit a then-high of $50 billion in 2008. The sector made up 18% of total industrial investment in Canada that year.Footnote i By 2009, the economic slowdown caused by the Global Financial CrisisFootnote 2 led to lower oil and gas demand, declining prices, and a rapid drop in Canadian oil and gas investment.

A recovered economy, and a rapid fall

After 2009, as the global economy recovered, so did demand for oil and gas. By mid-2014, Canadian oil and gas investments reached a new high of over $80 billion, with the sector’s share of total industrial investment also peaking that year at 24%. By late 2014 to early 2015, however, crude oil prices – and Canadian oil and gas investment – fell rapidly. This was due to a slowdown in global oil demand, and increased competition for market share amongst U.S. tight oilDefinition* producers and members and allies of OPEC.Footnote 3

A slow recovery, and a global pandemic

Oil prices and global investments began recovering in 2016, after OPEC and its allies struck a deal to restrict production and reduce inventories. That recovery lasted until early 2020, when the COVID-19 pandemic led to significantly reduced global economic activity and oil demand. By 2020, with annual average WTIFootnote 4 prices at US$40 per barrel, Canadian oil and gas investment fell to $24 billion, a level not seen since 2002. Investment in 2020 was down more than two-thirds from 2014’s peak, when WTI prices averaged US$90 per barrel. Also in 2020, Canadian oil and gas investments’ share of total industrial investment dropped to 7%, its lowest in close to three decades.

Investments differ by resource type

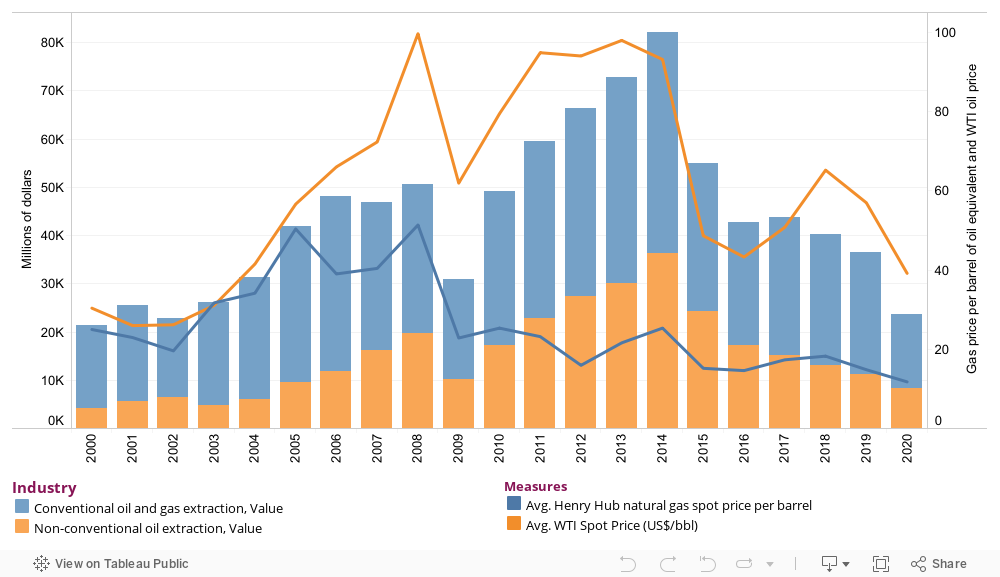

Canadian conventional oil and gas resource investment is generally more than double that for non-conventionalFootnote 5Footnote 6 (Figure 1). While Canadian oil and gas investment followed both oil and natural gas prices up to 2008, it has since followed oil prices more closely.

This is because of increased investing in Canadian oil sands, tight oil, and wet gas,Footnote 7 all of which follow oil prices. On the other hand, growing gas production from shaleDefinition* and other tight formations has kept North America’s continental natural gas market well-supplied, keeping prices relatively low since 2009, and reducing investment in Canadian dry gas.Definition*

Figure 1: Oil and gas prices and conventional and non-conventional investment

Data Source and Description

Data Source: StatsCan Table 36-10-0096-01, Energy Information Administration

Description: Conventional investment generally doubles non-conventional for the period represented in the chart, however, at the beginning of the twenty-first century it was at a four-to-one ratio for few years. While the relationship between oil price and investment continues, the relationship with gas prices weakened after 2008.

Investments differ by region

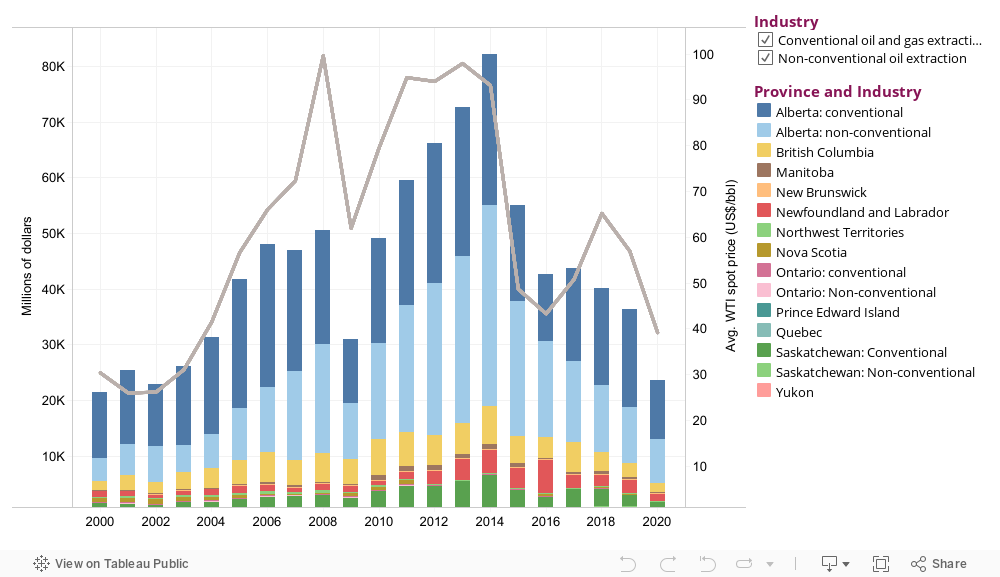

By province or territory, Alberta consistently received the largest share of investment in Canadian oil and gas, exceeding all the others combined – reflecting the availability of resources in the province relative to other regions in the country. Typically, most investment in oil and gas in Alberta flowed to conventional resources, though, from 2011 to 2016, most went into non-conventional resources in Alberta’s oil sands.

British Columbia, where Montney Formation tight gas resources have been the focus since 2009, often had the second-most investment in Canadian oil and gas. Investments in Saskatchewan oil and gas, in both conventional oil and gas and non-conventional thermal oil projects, typically rose and fell with oil prices. Investment in Newfoundland and Labrador was mainly offshore at the Hibernia, Terra Nova, White Rose, and Hebron oil fields. Across the rest of the country, oil and gas investment was relatively small.

Figure 2: Oil and gas investment by provinces and territories

Data Source and Description

Data Source: StatsCan Table 36-10-0096-01, Energy Information Administration

Description: Oil and gas investment mirrors oil price, increasing to 2008 then plunging in 2009 followed by a sharp recovery until 2014 before plunging again until 2020. Investment is dominated by Alberta, British Colombia, Saskatchewan and Newfoundland and Labrador. Non-conventional investment occurs only in Alberta and Saskatchewan while Ontario explored this option between 2002 and 2008.

High prices and rebounding investments

A post-COVID economic rebound combined with energy security concerns due to Russia’s invasion of Ukraine have led to higher oil and gas prices in 2021 and 2022. Following a trend of higher prices, Statistics Canada’s latest Annual Capital Expenditures Survey data indicates that Canadian oil and gas investment levels in 2022 are likely to be one-third higher than the 2020 lows.Footnote ii

Other factors influence investment

Future capital spending will depend on many complex factors, such as technology, investment, and policy trends. For example, energy companies face new challenges as availability and allocation of funds is increasingly impacted by ESG considerations – including net-zero emissions policies around the world. Meanwhile, Canadian oil and gas companies may not choose to reinvest growing cashflows in new production capacity but instead pay back debt, their investors (via dividends), or repurchase their shares, as well investing in technology which can help achieve operational efficiencies, reducing input costs, energy use, and emissions to comply with public policy objectives and regulations. Therefore, even though higher prices are leading to new investments, non-price factors are likely to become more important in determining future investment and production trends in Canada’s oil and gas sector.

- Date modified: