Market Snapshot: East Coast LNG Projects Tackle Competition and Supply Challenges

Release date: 2015-08-27

Due to growing natural gas production in North America, 27 companies have applied to the NEB for a licence to export natural gas since 2010. There are a number of liquefied natural gas (LNG) export projects proposed for both the east coast and the west coast of Canada, all of which compete with each other and with other projects around the world to meet growing LNG demand, which averaged approximately 32 billion cubic feet per day (Bcf/d) in 2014. In addition to proposed projects in Canada, approximately 10 Bcf/d of export capacity is already under construction in the U.S. and various Australian projects will be commissioned in late 2015 and 2016, significantly increasing global LNG supply.

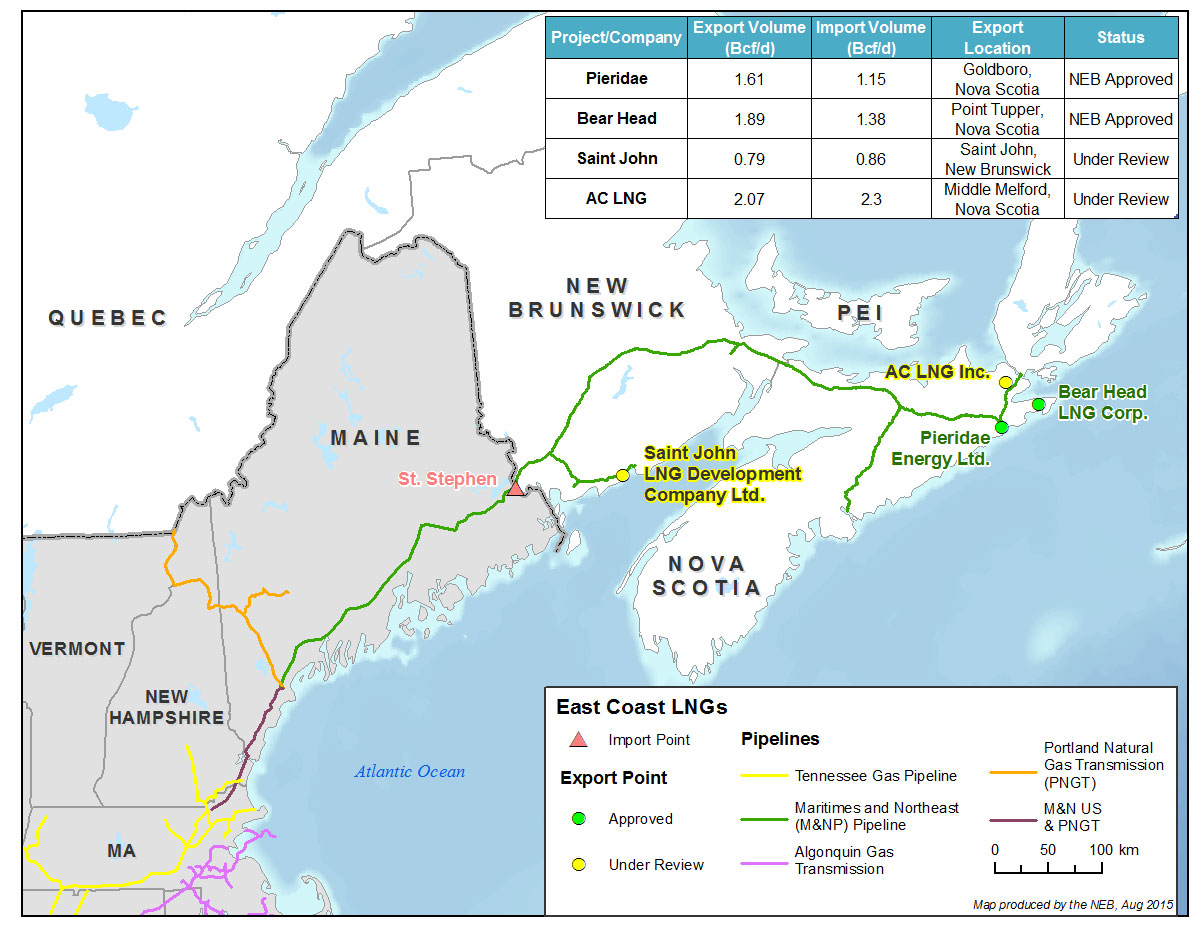

There are four projects which would export LNG from the Maritimes with a combined export volume of 6.4 Bcf/d. The Board recently approved natural gas export licenses for two of the projects and two have applications before the BoardFootnote 1. As a condition of each export licence recently granted, if exports from Canada do not commence within 10 years from the issuance of the licence, the licence will expire.

Proposed East Coast Liquefied Natural Gas Export Projects

Figure Sources and Description

Sources: Applicants’ Export Licence Applications and Project Descriptions, NEB

Description: The map shows the four proposed LNG export projects from the east coast of Canada, and the Maritimes and Northeast Pipeline system. It includes a chart displaying the applied-for and approved import and export licence volumes, exports points and status of each application filed with the Board.

In addition to the challenge of global competition, LNG exporters from the Maritimes face the challenge of finding long-term sources of natural gas supply. The four Maritimes LNG export Applicants (see map above) cited several sources of supply to support their projects, including Maritimes onshore and offshore production, as well as supply from Western Canada and the Marcellus formation in the U.S. Northeast. According to the U.S. Energy Information Administration, Marcellus production is currently averaging over 16 Bcf/d, a significant increase from less than 2 Bcf/d in the late 2000s. Although Maritimes supply was included, 2015 natural gas production in the Maritimes averaged 0.25 Bcf/d and is expected to decline.

The Maritimes natural gas market is connected with the U.S. via the Maritimes & Northeast Pipeline (M&NP). The current capacity of the Canadian portion of M&NP is approximately 0.6 Bcf/d, and is insufficient to transport all the volumes proposed to be exported from the Maritimes. Moreover, ongoing pipeline bottlenecks in the U.S. are currently preventing U.S. Northeast supply from reaching Maritimes consumers. Should Maritimes LNG projects proceed, additional infrastructure may be required to service the LNG plants.

- Date modified: