Market Snapshot: Ethane potential from natural gas production is significant and is expected to continue to grow in Canada

Release date: 2019-07-10

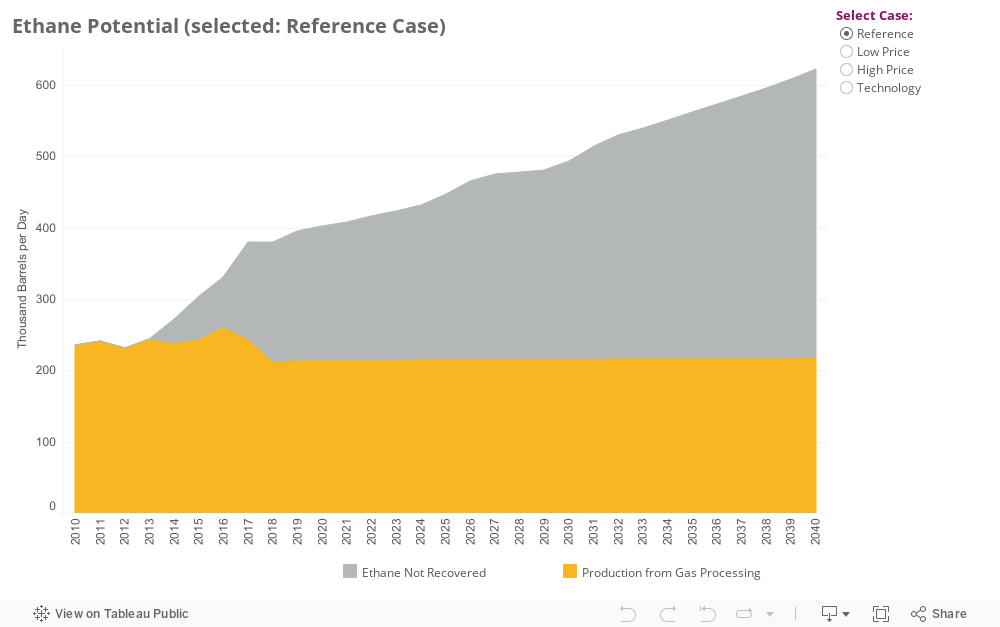

Production of liquids-rich natural gas has grown over the last six years in Canada, increasing potential natural gas liquids (NGL) supply, including ethane. However, not all ethane present in the gas stream is recovered because Canadian ethane demand is limited. The figure below shows ethane potential broken into the amount of ethane that is produced and the amount of ethane that is not recovered. Importantly, ethane potential—especially unrecovered ethane—is projected to continue growing as natural gas production grows.

Figure 1: Projected Ethane Potential through 2040

Source and Description

Source: NEB

Description: The stacked area chart shows projected ethane potential until 2040. This includes ethane produced from gas processing and ethane not recovered. In 2010, Canadian ethane potential was 236 thousand barrels per day (Mb/d), with all of it produced from gas. In 2018, Canadian ethane potential was 380 Mb/d, with 168 Mb/d not recovered. The following numbers are some of the projections in each case:

- Reference Case: In 2025, Canadian ethane potential is projected to be 447 Mb/d, with 231 Mb/d not recovered. In 2040, Canadian ethane potential is projected to be 622 Mb/d, with 404 Mb/d not recovered.

- Low Price Case: In 2025, Canadian ethane potential is projected to be 366 Mb/d, with 150 Mb/d not recovered. In 2040, Canadian ethane potential is projected to be 385 Mb/d, with 165 Mb/d not recovered.

- High Price Case: In 2025, Canadian ethane potential is projected to be 478 Mb/d, with 264 Mb/d not recovered. In 2040, Canadian ethane potential is projected to be 779 Mb/d, with 562 Mb/d not recovered.

- Technology Case: In 2025, Canadian ethane potential is projected to be 428 Mb/d, with 213 Mb/d not recovered. In 2040, Canadian ethane potential is projected to be 416 Mb/d, with 196 Mb/d not recovered.

Figure 1 includes projections of ethane potential for all four Canada’s Energy Future 2018 cases. Even with lower natural gas production in the Low Price Case, ethane potential is significantly higher than ethane production. This implies room for additional petrochemical demand for ethane to develop in western Canada. The majority of ethane disposition is petrochemical demand in Alberta and Ontario. While Alberta’s petrochemical capacity expanded in 2016, future expansions are uncertain, so their capacity is held constant. Ontario’s petrochemical capacity will increase over the next few years, but since there is no domestic supply of ethane in eastern Canada, imports into Ontario from Pennsylvania and Ohio supply the demand.

For additional information see Canada’s Energy Future 2018 Supplement: Natural Gas Liquids Supply and Disposition.

- Date modified: